")

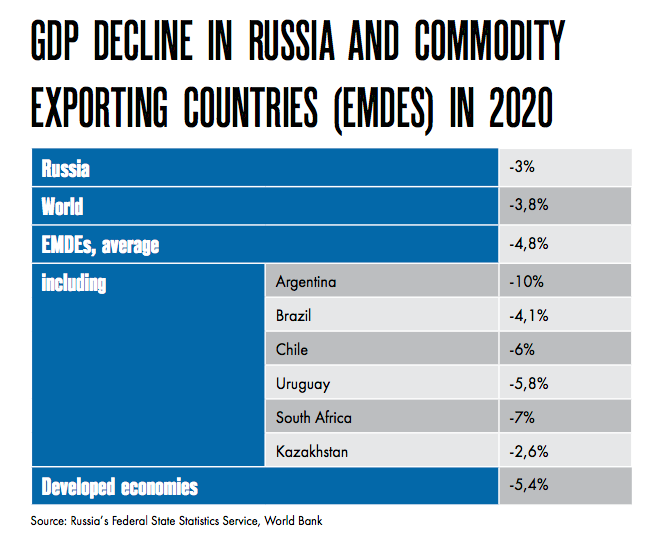

The World Bank’s latest Russia Economic Report suggests Russia has been less affected by the corona crisis than Europe or other commodity-driven economies. In 2020, Russia’s GDP fell by 3.0% compared to contractions of 4%-6%, and some even 10%, in other economies. That difference was due to several factors that helped Russia perform relatively better.

“In recent years, the country has undertaken significant macro-fiscal stabilization efforts, resulting in an improved fiscal position. Among other contributing factors were enhanced regulation and supervision in the banking sector, fortified capital and liquidity buffers, relatively soft restrictions for industrial and construction sectors, closer ties to

a relatively fast-growing China, a relatively small services sector and a large public sector that buffered against unemployment,” said Apurva Sanghi, the Lead Economist for the World Bank in Russia.

Major budget deficit avoided

The measures taken by the government and the Central Bank towards macro-fiscal stability have led to significant improvements in the fiscal sphere compared to 2013. The federal budget non-oil primary deficit reached 4.7% of GDP, compared to 9.7% in 2013, the World Bank experts highlighted. Over that time, the country achieved a sizeable accumulation of fiscal and reserve buffers (as of July 1, 2021, the National Wealth Fund reached RUR 13.575 tln ($185.8 bln) while its liquid part was about RUR 8.313 tln ($116.4 bln, or 7.2% of GDP).

International reserves at the end of June 2021 stood at $592.4 bln, a level the World Bank experts described as ‘comfortable.’ In 2020, this type of reserves increased by 7.5% to reach $595.8 bln as of January 1. Russia’s international reserves reached an all-time high of $605.9 bln on May 28, 2021.

Due to the so-called fiscal rule that regulates channeling revenues into the NWF, as well as the investment of international reserves consisting of monetary gold, special drawing rights (SDR) holdings, reserve position in the IMF, and foreign currency, Russia could reduce exposure to oil price volatility and lower its public debt burden to RUR 19.7 tln ($270 bln), or 17% of GDP, as of June 2021. In fact Russia’s debt burden remains substantially lower than in other commodity-dependent economies, where it reaches 63% of GDP. The cost of servicing the public debt in Russia is 1% of GDP against 2% of GDP in other developing countries.

Enhanced banking sector regulation and supervision

The World Bank believes the massive banking sector ‘clean-up’ the Central Bank has been implementing for the past few years has borne fruit and ‘fortified capital and liquidity buffers.’ These efforts strengthened Russia’s ability to respond to the pandemic’s most adverse economic shocks.

In 2020, the Russian government provided a substantial countercyclical fiscal stimulus, about 4.5% of GDP, comparable with the amount of anticrisis support for businesses in other developing countries. In 2021, the country plans to spend approximately 1.1% of GDP for these purposes.

For reference, during the pandemic, Russia adopted three packages of measures to support Russian businesses, as well as the National Economic Recovery Plan approved by the government in October 2020. The plan includes over 500 support measures targeting businesses and individuals; its success criterion is unemployment below 5% at the end of 2021, and annual GDP increase at least at 3%. According to the World Bank forecast, these targets are quite achievable in Russia.

Ties with China have kept the Russian economy afloat

Russia’s close economic links with China are yet another significant factor that contributed to the relatively low GDP decline rate. Even amid the corona crisis, China showed a cyclical economic growth and its GDP never dropped, unlike in other countries. China’s GDP stood at 2.3% as of 2020.

Experts note that even during the crisis, the growth of the Chinese economy was fueled by a high demand for Chinese products both domestically and abroad. Government investment also stimulated economic activity.

“Our trade with China is recovering. Exports to China were affected the least by the crisis. Imports from China between January and October 2020 were even higher than during the same period in 2019. This is probably due to China’s swift recovery from the pandemic: Chinese exporters are already trying to actively scale up their businesses while in many other countries, companies continue to be paralyzed by COVID-19 restrictions,” says Anton Tabakh, Managing Director for Macroeconomic Forecasting of the Expert RA rating agency.

There are wider opportunities for e-commerce, and the Chinese government supports international logistics through subsidies for railroad container shipments, which makes Chinese products even more attractive to the global retail and end customers. As of 2020, Russia’s trade with China exceeded $100 bln, in a trend persisting for three consecutive years.

Prevalence of state-owned companies helped

Oddly enough, the Russian economy benefited from large state corporations dominating the structure of domestic business. According to the Federal Anti- Monopoly Service, the share of the added value created by state companies in Russia’s GDP is now around 65%. Private businesses and consumer services are the sectors hit the hardest by the pandemic everywhere in the world. Since in Russia, these sectors account for a relatively small share of GDP (22%, with developed countries having 40–50%), the overall recession has been lower than in other countries. The public sector, which has been less vulnerable to the direct effects of the COVID-19 restrictions, also provided certain protection from unemployment.

The World Bank’s prognosis: Everything will be fine (but will it though?)

According to the World Bank’s forecast, in 2021 the global GDP will be growing despite the persisting strong impact of the pandemic on all business processes. By the end of 2021, the world economy is expected to grow by 5.6%, the highest recovery rate after a recession in the past 80 years.

The United States will see an economic growth of 6.8% this year as an effect of large-scale support measures from the federal budget and lifted lockdown restrictions. China will be the country to show the most impressive economic upturn (8.5%) among countries with emerging markets and developing economies. It will bounce back thanks to the deferred demand being satisfied by the Chinese population and consumers of Chinese products around the world.

As to emerging markets and developing countries, their economies are expected to grow by 6%. However, with China excluded from the overall statistics, the indicator would be much more modest, only 4.4%. In 2022, the economic recovery rate in these countries will reach 4.7% — yet, this will not be sufficient to compensate for the losses they suffered in 2020, with the next year’s production volumes expected to slump by 4.1% as compared to pre-pandemic forecasts.

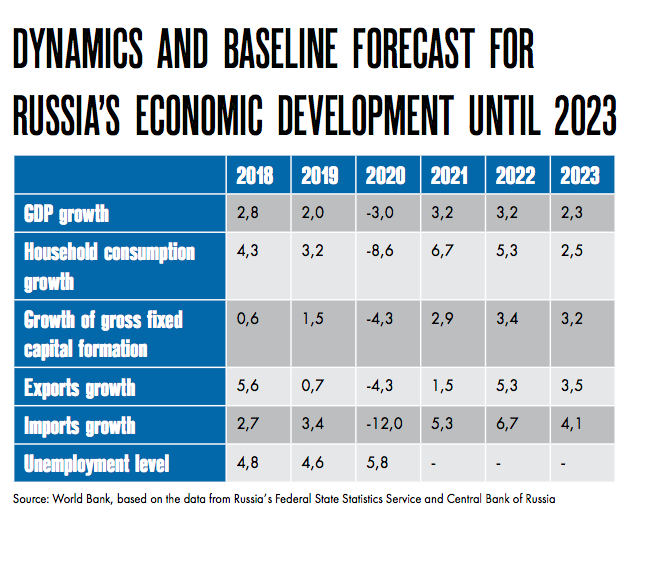

Russia’s GDP growth: three scenarios

According to the World Bank’s baseline forecast, Russia’s GDP growth in 2021, 2022 and 2023 will account for 3.2%, 3.2% and 2.3%, respectively. The recovery of the Russian economy, supported by a growth in household consumption and investments, is expected to be stimulated by the global economic recovery, increased oil prices, and mild monetary conditions in the domestic market in 2021.

By late 2021-early 2022, we may see a resumption of migration flows, which will also have a positive effect on investment projects that are currently lacking labor force, such as the expansion of the Baikal-Amur Mainline (BAM) and the Trans-Siberian Railway, the largest investment project implemented by Russian Railways in the next few years, whose plans for this year include involving military railway servicemen and even prisoners due to a lack of migrants; however, these efforts will not fully satisfy the project’s demand for workforce.

The optimistic scenario assumes acceleration of Russia’s GDP growth in 2021, 2022 and 2023 up to 3.8%, 4.8% and 3.3%, respectively, as well as a more rapid increase of domestic demand than expected in the baseline scenario. Such developments are possible in case we see the impacts of the pandemic overcome faster than assumed in the baseline scenario, oil prices growing more actively in the world market, and the government providing a more expansive support to businesses affected by the coronavirus crisis as well as to the poorest groups of the population.

Under the pessimistic scenario, we might expect GDP growth in 2021, 2022 and 2023 at 2.6%,—0.7% and 0.6%, respectively, while investment volumes will decline in 2022–2023. New COVID-19 outbreaks together with ineffectiveness of vaccination against new coronavirus strains and new sanctions imposed against the Russian economy by other countries may slow down the economic recovery.

“The short-term economic recovery will depend on the outcome of efforts to tackle the pandemic, while in the long term, the key condition for economic advancement will be the acceleration of potential growth through stimulating economic diversification, creating a level playing field for the private sector, improving governance quality, particularly as regards state enterprises, as well as seizing opportunities that allow for changes in global value-added chains,” — World Bank analysts concluded.